Introduction to the 50/30/20 Rule

The 50/30/20 budget rule is one of the simplest and most effective money-management strategies used by Americans today. It gives you a clear plan to divide your after-tax income into needs, wants, and savings—without stressing over complicated spreadsheets or formulas.

Why This Budgeting Rule Is So Popular

People love it because it’s easy, flexible, and works for almost everyone. Whether you’re living paycheck to paycheck or trying to build wealth, this method helps you create balance in your financial life.

Who Should Use This Method?

Anyone who wants a simple structure for budgeting—students, families, young professionals, or even retirees—can use the 50/30/20 rule. It’s especially helpful if you struggle with overspending or saving consistently.

Breaking Down the 50/30/20 Budget Rule

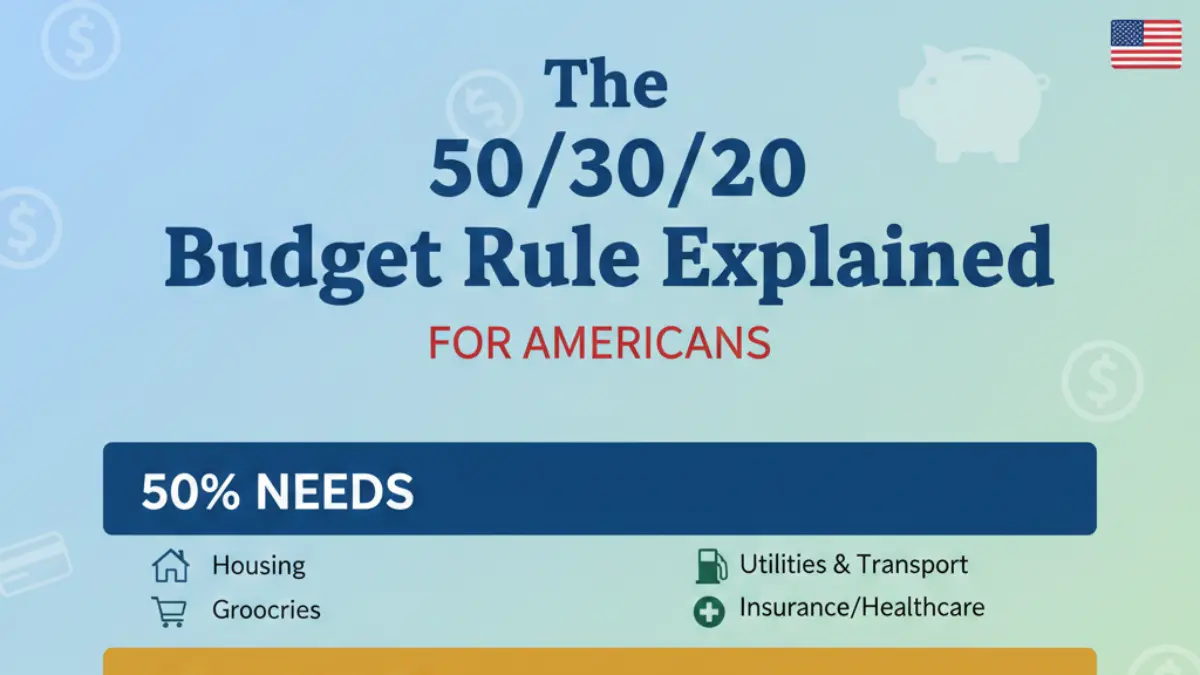

The 50%: Needs Explained

Needs are essential expenses you must pay to survive and function. These include:

- Rent or mortgage

- Utilities

- Groceries

- Car payments

- Insurance

- Minimum loan payments

- Medical expenses

If your needs go above 50%, don’t panic—it just means adjustments will be necessary.

The 30%: Wants Explained

Wants are the fun things in life—things you can live without but enjoy:

- Restaurants and takeout

- Streaming subscriptions

- Shopping

- Vacations

- Gym memberships

- Entertainment

These expenses add joy, but keeping them under control is key.

The 20%: Savings & Debt Repayment Explained

This portion strengthens your financial foundation. It includes:

- Emergency fund

- Retirement contributions

- Extra payments toward loans

- Investments

- Big savings goals like home down payment

Examples of Each Category

| Category | Example Items |

|---|---|

| Needs | Rent, groceries, utilities |

| Wants | Movies, travel, eating out |

| Savings | 401(k), Roth IRA, emergency fund |

How the 50/30/20 Rule Helps Americans Manage Money

Reducing Overspending

Knowing exactly how much to spend in each category helps you avoid impulse purchases and unnecessary expenses.

Building a Strong Savings Habit

The rule forces you to set aside 20% consistently, helping you build wealth over time—even if your income isn’t very high.

Makes Budgeting Easy for Beginners

You don’t need finance expertise to follow this rule. Just divide your income, track expenses, and adjust when needed.

Step-by-Step Guide to Applying the Rule

Step 1: Calculate Your After-Tax Income

Use your pay stub to determine how much you actually bring home after taxes, Social Security, and other deductions.

Step 2: Divide Your Income Into Categories

- 50% → Needs

- 30% → Wants

- 20% → Savings

Step 3: Track Your Spending

Use an app or simple notebook. Tracking makes you aware of overspending patterns.

Step 4: Adjust Monthly

Budgets are not permanent. Review and adjust monthly based on lifestyle changes.

Real-Life Example of the 50/30/20 Rule

Income Scenario: $4,000 Per Month

Let’s break it down:

Needs Breakdown (50% = $2,000)

- Rent: $1,200

- Groceries: $400

- Utilities: $200

- Insurance: $200

Wants Breakdown (30% = $1,200)

- Eating out: $300

- Shopping: $200

- Entertainment: $200

- Travel savings: $500

Savings Breakdown (20% = $800)

- Emergency fund: $300

- Retirement savings: $300

- Debt repayment: $200

Benefits of the 50/30/20 Budget Rule

Simple and Beginner Friendly

Anyone can start it within minutes.

Helps Reduce Debt Faster

With 20% dedicated to savings and debt repayment, you can pay off loans sooner.

Encourages Financial Discipline

It builds money awareness and long-term financial responsibility.

Limitations of the 50/30/20 Rule

Not Ideal for High Cost-of-Living Areas

Cities like New York or San Francisco make it hard to keep needs below 50%.

Not Suitable for Irregular Income

Freelancers or commission-based workers need more flexible budgeting methods.

May Need Adjustments Over Time

Lifestyle changes, new goals, or emergencies require modifications.

How to Customize the Rule for Your Lifestyle

Adjusting for High Rent or Bills

If your rent takes up more than 50%, reduce your wants category.

Adjusting for Savings Goals

Increase the 20% savings section if you’re saving for a house, wedding, or retirement.

Adjusting for Debt Payments

If you’re aggressively paying off loans, allocate more toward the 20% category.

Best Tools and Apps to Use for This Rule

Mint

Tracks your spending automatically.

YNAB (You Need A Budget)

Perfect for detailed budgeting.

Personal Capital

Great for tracking investments and net worth.

EveryDollar

A simple zero-based budgeting tool.

Common Mistakes Americans Make While Budgeting

Misidentifying Wants as Needs

Buying a new iPhone isn’t a need—it’s a want.

Ignoring Small Expenses

Small daily purchases like coffee add up fast.

Not Updating the Budget Regularly

Life changes—your budget should too.

Tips to Stay Consistent With the 50/30/20 System

Automate Savings

Let your bank transfer money automatically each month.

Use Cash for Wants

Cash helps you control overspending.

Review Spending Weekly

Weekly reviews prevent month-end surprises.

Conclusion

The 50/30/20 rule is one of the simplest and most effective budgeting methods for Americans. Whether you’re trying to save more, reduce debt, or simply build control over your money, this method gives you a clear and manageable structure. It’s flexible, beginner-friendly, and helps you stay consistent with your financial goals. With the right adjustments and tools, anyone can make this system work for their lifestyle.

FAQs

1. Is the 50/30/20 rule realistic for low-income Americans?

Yes, but it may require adjusting percentages to fit essential needs.

2. Can I use the rule if I live in a high-rent city?

Yes, but you’ll likely need to shift more toward the “needs” category.

3. Should I include taxes in the budget rule?

No, the rule applies to after-tax income.

4. Can I use this rule if I have a lot of debt?

Absolutely—allocate more to savings/debt repayment if needed.

5. Is the rule good for beginners?

Yes, it’s one of the easiest budgeting methods for beginners.