Introduction

Building credit in the USA can feel like trying to get a job without experience—they want experience, but you need the job to get it. The credit system works the same way. If you’re new to the country, young, or simply haven’t used credit before, starting from zero can be confusing. The good news? There are proven, simple methods to build your credit from scratch quickly and safely.

Let’s break it down step by step.

Introduction to Building Credit

Why Credit Matters in the USA

Credit affects almost everything in the United States—your ability to rent an apartment, buy a car, get a mortgage, or even qualify for certain jobs. A good credit score shows lenders that you’re trustworthy and responsible with money.

Challenges of Starting with No Credit History

No credit means lenders can’t predict how you’ll handle debt. So they treat you as “high risk” until you prove otherwise. But with the right tools, you can build credit efficiently without falling into debt traps.

Understanding the Basics of Credit

What Is a Credit Score?

A credit score is a three-digit number, usually between 300 and 850, that measures your creditworthiness. The higher the score, the better your chances of getting approved for loans with low interest rates.

What Impacts Your Credit Score?

Payment History

This makes up 35% of your score. Paying bills on time is the number one rule.

Credit Utilization

How much of your credit limit you use. Keep it under 30%, ideally under 10%.

Length of Credit History

The longer you have an open and active account, the better.

Credit Mix

Having different types of credit—like a card and a loan—boosts your score.

New Credit Inquiries

Applying for too many accounts at once lowers your score temporarily.

Best Ways to Build Credit from Scratch

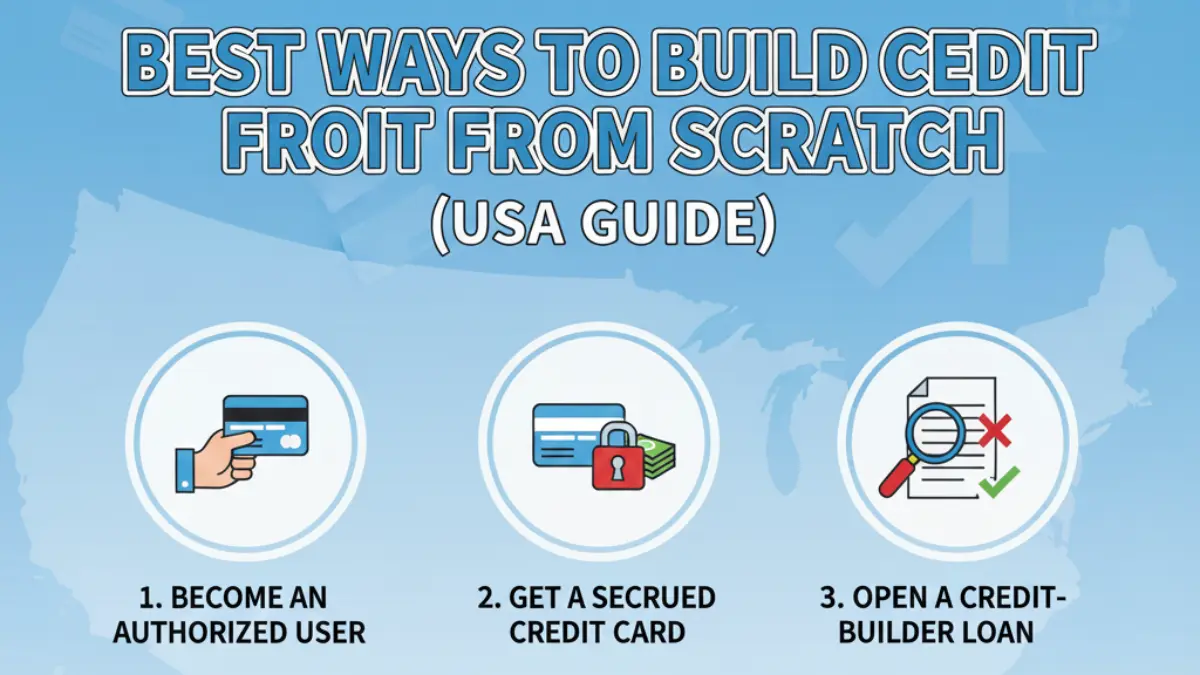

Get a Secured Credit Card

This is one of the easiest ways to start. You deposit money (usually $200–$500), which becomes your credit limit. Use it for small purchases and pay the balance in full every month.

Apply for a Credit-Builder Loan

Offered by credit unions and some online lenders, these loans hold the borrowed amount in a savings account while you make monthly payments. Once you finish paying, you get the money back—and a better credit score.

Become an Authorized User

Ask a trusted family member with good credit to add you to their card. Their positive history will help your score grow without you needing your own credit line.

Use a Co-Signer for Your First Credit Account

A co-signer shares responsibility for the loan. If you don’t qualify alone, this gives you a boost. But make sure you never miss payments, or both credit scores suffer.

Report Your Regular Bills to Credit Bureaus

Rent, phone bills, utilities—these payments usually don’t count toward credit unless you use services like:

- RentTrack

- eCredable

- Your landlord’s reporting program

Use Alternatives Like Self or Experian Boost

Tools like Self help you build credit through installment plans, while Experian Boost counts your streaming, utilities, and phone bill payments toward your Experian credit score.

Smart Credit Habits to Build a Strong Foundation

Pay Every Bill On Time

Think of on-time payments as your “credit reputation.” Even one missed payment can drag your score down for months.

Keep Credit Utilization Low

Just because you have a limit of $500 doesn’t mean you should use $450 of it. High usage signals risk.

Avoid Applying for Too Much Credit

Each new credit application triggers a “hard inquiry.” Too many in a short time looks desperate to lenders.

Monitor Your Credit Regularly

Use free tools like Credit Karma, Experian, or your bank’s credit tracker. Spot mistakes early and dispute inaccuracies.

Mistakes to Avoid When Building Credit

Closing Your First Credit Accounts Too Early

Old accounts help your score. Keep them open unless they charge heavy fees.

Missing Payments

Missing even one payment can tank your score by 60–100 points.

Overspending With New Credit

Credit is a tool, not free money. Overspending leads to debt, fees, and a damaged score.

How Long It Takes to Build Credit

Realistic Timeline

Most people see their first credit score in 3–6 months after opening an account.

Factors That Speed Up or Slow Down Progress

- Using credit responsibly speeds things up.

- High utilization, missed payments, or too many applications slow progress.

Conclusion

Building credit from scratch in the USA doesn’t have to be complicated. With smart decisions—like getting a secured card, paying bills on time, keeping balances low, and using credit-building tools—you can create a strong financial foundation within months. Start small, stay consistent, and remember that credit building is a marathon, not a sprint.

FAQs

1. How fast can I build credit from zero?

Usually within 3–6 months you’ll have a score.

2. Do rent payments count toward credit?

Yes, but only if you use a rent-reporting service.

3. Is a secured credit card safe for beginners?

Absolutely. It’s one of the best tools for new credit builders.

4. Will checking my credit lower my score?

No—checking your own score is a soft inquiry.

5. What’s the easiest way to start building credit?

A secured credit card or becoming an authorized user are the most beginner-friendly options.